- Review of Commissioning in 2024

In 2024, China commissioned 17 cold-rolled and coated steel production lines, with a total capacity of approximately 8.39 million mt. Among these, three were cold-rolling lines with a capacity of 3.96 million mt, and 14 were coated steel lines with a capacity of 4.43 million mt. Regionally, east China and north China remained the primary contributors to the new cold-rolled and coated steel capacity.

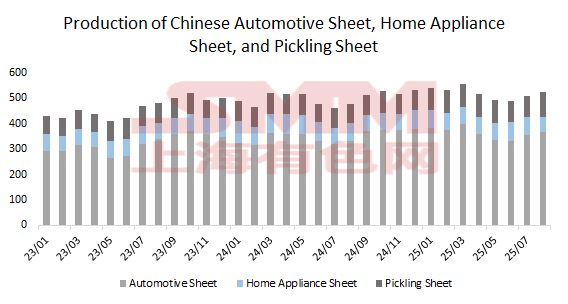

In recent years, the capacity and production of cold rolling have grown rapidly. The reasons behind this trend are, on one hand, related to the strong demand support from downstream industries such as automobiles and home appliances. In China, the production of automotive sheets and home appliance sheets has continued to increase.

On the other hand, it is also due to the transformation of China's steel capacity landscape. Since H2 2021, the sharp downturn in the real estate sector has led to a rapid contraction in the production and profits of construction steel, prompting the market to shift its focus to sheets & plates products with greater demand potential. However, following active capacity commissioning by multiple steel mills from 2023 to 2024, overcapacity in hot-rolled coils intensified rapidly, resulting in fierce competition among suppliers. Hot-rolled coil prices were forced into a "price war," and profit margins narrowed accordingly. In contrast, cold-rolled products and their deep-processing derivatives still maintain relatively attractive profit margins at this stage, which is the key reason why considerable cold-rolled capacity has continued to be commissioned over the past three years.

- Commissioned and Planned Commissioning in 2025

From January to September 2025, according to SMM, 10 cold coating lines were commissioned domestically, involving a capacity of approximately 7.55 million mt. Most of these projects were located in north China and east China markets, with products primarily positioned in the high-end coated steel segment.

Medium and long-term, several additional lines remain under construction, though their commissioning times have yet to be determined. SMM will continue to monitor these developments over the long term.

![[SMM Steel] India emerges as net exporter of finished steel in Apr-Feb FY26](https://imgqn.smm.cn/usercenter/UqlZJ20251217171717.jpg)

![[Domestic Iron Ore Commentary] Iron Ore Concentrates Prices in the Tangshan Area May Have Some Upside Potential](https://imgqn.smm.cn/usercenter/HbWNv20251217171718.jpg)